UK MARKET PERFORMANCE – Same Store Sales (SSS) Overview

Performance during 2026W7 (Week ending 02/15/2026)

Total Restaurant Cohort:

SSS: +1.2% YoY | +19.3% vs prior week

Indicates a strong WoW rebound across the market.

Fine Dining:

SSS: +4.4% YoY | +26.3% vs prior week

Outperformed the broader market on both YoY and WoW metrics.

Upscale Casual:

SSS: –2.1% YoY | +14.3% vs prior week

Still below last year but showing meaningful week‑over‑week recovery.

PERFORMANCE DRIVERS

Higher Sales per Head (SPH) is the primary driver of positive sales momentum. SPH increases helped offset the traffic softness.

Total Cohort: SPH +1.5% YoY | Avg SPH £54.2

Fine Dining: SPH +5.1% YoY | Avg SPH £104.2

Upscale Casual: SPH +5.2% YoY | Avg SPH £41.2

The week reflects stronger spend per guest despite softness in cover volumes.

OBSERVATIONS

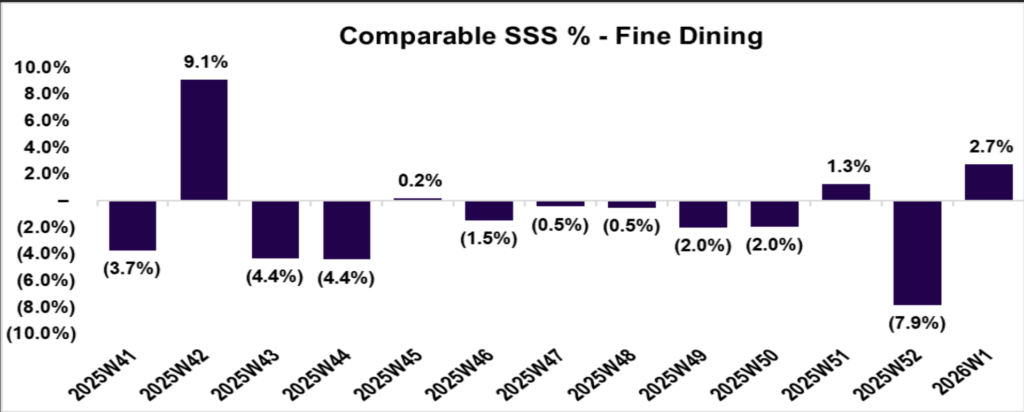

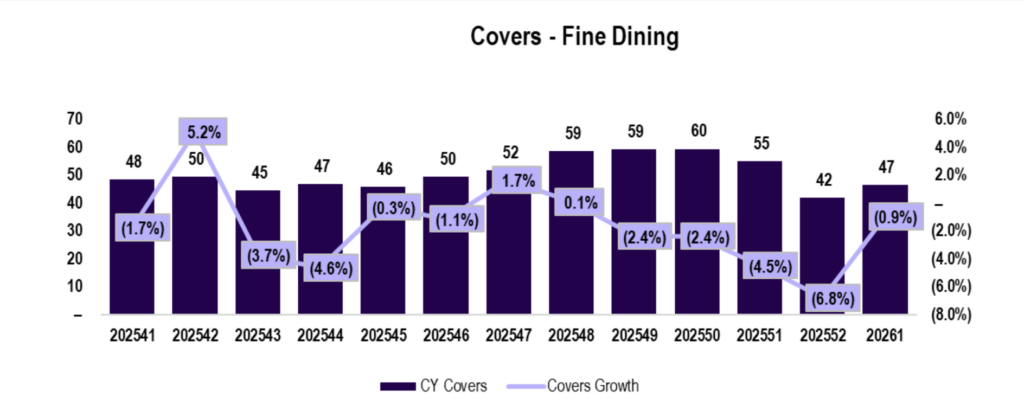

Over the trailing 13‑week period (2025W41 to 2026W1), Our Fine Dining portfolio experienced a SSS decline of ~ (1.0%) versus the prior year, driven primarily by a ~ (1.7%) drop in traffic.

Consumers have been scaling back on dining‑out occasions – particularly higher‑priced, family‑oriented meals. Notably, 46% reported plans to reduce how often they dine out, which has directly affected hotel family‑meal traffic and event‑catering volumes. (1) This shift in consumer behavior has contributed to the softer performance in both Fine Dining and Family Dining.

(1) Leisure and hospitality industry outlook 2025 | RSM UK